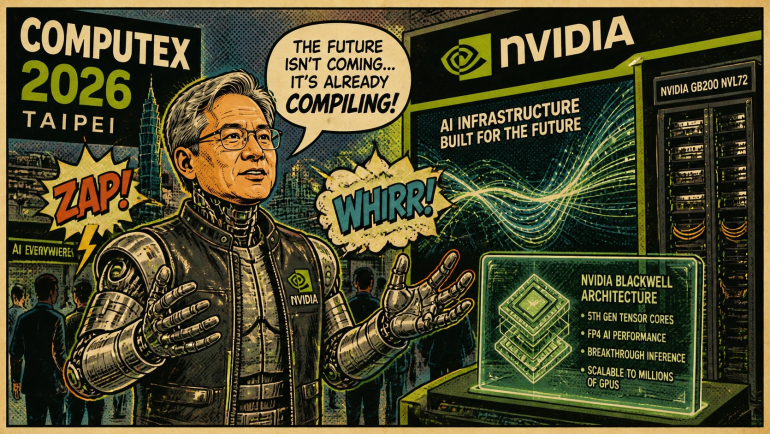

Computex 2026 in Taipei is shaping up as this year’s most important AI confab for investors, where silicon dreams, data centers, and “agentic” robots all compete to see who can justify the fattest forward multiples.

The Street Goes to Taipei

Wall Street likes to think of itself as the world’s center of gravity, but for one week in early June the pole shifts about 6,400 miles west to Taipei. Computex 2026, the long-running tech trade show that once obsessed over motherboards and beige boxes, has recast itself as a global summit on artificial intelligence, accelerated computing, and what vendors now call “AI factories.” The rebrand comes with a theme—“AI Together”—and a guest list of chipmakers, cloud platforms, and upstart infrastructure vendors all eager to convince investors that they are indispensable in the coming AI economy.

For portfolio managers, the event has become less of a gadget fair and more of a forward‑looking earnings call conducted at stadium volume. The booths might be in Taipei’s Nangang and Xinyi districts, but the audience, judging by the valuation chatter, is sitting on trading floors in New York, London, and Singapore.

From PC Show to AI Factory Floor

Computex started life in 1981 as an information and communications technology bazaar, a place to survey the full PC and component supply chain in one jet‑lagged lap. Taiwan’s dense industrial clusters turned the show into a barometer for hardware cycles: more laptops and routers one year, more servers and motherboards the next.

Today, the event’s organizers describe it as a “global benchmark” for AI and startups, with this year’s show bringing together roughly 1,500 exhibitors across 6,000 booths—numbers that would make most investor conferences look like a small‑cap roadshow. The focus now spans AI and computing, robotics and mobility, and a grab bag of “next‑gen tech,” shorthand for anything that might justify another turn of the multiple.

Jensen’s World: AI at Stadium Scale

This year, one of the marquee attractions isn’t on the show floor at all but on stage at the Taipei Music Center, where Nvidia (NVDA) chief executive Jensen Huang is scheduled to deliver a keynote as part of an adjacent GTC Taipei event. The company bills it as a tour of “AI factories and scaling infrastructure,” the kind of phrasing that makes data centers sound less like buildings and more like money‑printing machines.

The semantics matter. “AI factory” implies a production system that converts capex into recurring intelligence, a comforting metaphor for investors hunting for durable free‑cash‑flow stories in a market that has already repriced anything with “GPU” in its slide deck. With Huang’s appearances now treated by some funds as quasi‑macro events, the Computex keynote doubles as a sentiment check on whether the AI infrastructure cycle can remain in “up and to the right” territory for another year.

Edge, Physical AI, and the Robots That Want Your Job (In a Good Way)

On the exhibitor floor, the AI story is fragmenting into niches, each promising to be the missing layer in someone else’s stack. ADLINK, a Taiwan‑based industrial computing firm, arrives touting “Physical AI” and edge AI agents, a phrase that sounds like science fiction until you notice the robots scanning shelves, inspecting parts, and politely threatening to obviate a few low‑margin workflows. Its booth, in the Industrial IoT and Embedded Systems zone, leans into manufacturing and healthcare use cases, the kind of operational‑efficiency stories CFOs like to hear when they are asked for another round of AI budget.

Nearby, other vendors push their take on edge intelligence, positioning themselves as the complement to hyperscale data centers rather than the competition. The subtext is clear: if AI truly migrates from a handful of cloud regions to every warehouse, clinic, and retail aisle, the companies wiring up the “boring” endpoints may enjoy some of the most durable growth.

Turning Compute Into a “Real” Economy

In the software aisles, the buzzword of choice is “compute economy.” INFINITIX, an AI infrastructure software provider, is using Computex to promote a three‑layer architecture it says turns raw compute into a commercial platform: infrastructure at the bottom, an AI platform in the middle, and cloud‑style services on top. The pitch is that its AI‑Stack and ixCSP products help enterprises both govern their GPU resources and sell them as services, a nod to the idea that unused cycles are as wasteful as empty airline seats.

If that sounds esoteric, remember that Wall Street has already learned to value businesses on metrics like “GPU hours consumed” and “tokens processed.” The notion that compute capacity could be flexibly packaged, monetized, and traded appeals to investors accustomed to slicing telecom bandwidth and cloud storage into recurring revenue streams. In the halls, one hears a familiar refrain: AI is no longer just a capex line; it is a product.

ASUS, ROG, and the Consumer Side of AI

Not everything at Computex is aimed directly at CIOs and data‑center architects. ASUS, along with its long‑running Republic of Gamers (ROG) brand, plans an extensive showcase highlighting AI‑infused devices for both enterprise and everyday use, while also marking ROG’s 20th anniversary in gaming hardware. The company’s booth at Taipei Nangang Exhibition Center puts AI‑enhanced laptops, edge devices, and gaming systems front and center, a reminder that the consumer side of AI still matters for volumes and brand affinity.

For investors, these demos serve as a reminder that AI demand doesn’t flow in a straight line from cloud to chipmaker. It also depends on whether consumers and prosumers perceive meaningful value in the “smarter” devices arriving on store shelves, from battery life and frame rates to AI‑assisted workflows. If the next generation of AI PCs and gaming rigs can command pricing power, that could ripple back through component suppliers and foundries alike.

Why This Matters for Portfolios

Computex has always been a place to gauge where the hardware cycle is headed, but in its AI‑centric incarnation it doubles as a cross‑section of the entire value chain—from chip design and manufacturing to cloud platforms, edge devices, and vertical applications. For investors, that makes Taipei a useful, if crowded, field trip.

Several themes stand out:

The show’s “AI Together” framing reinforces the idea that no single vendor owns the stack; interoperability and ecosystem positioning matter as much as raw performance specs.

The sheer scale—1,500 exhibitors and 6,000 booths—suggests that competition will intensify not just at the high end of GPUs, but across middleware, orchestration, and edge deployments.

The emergence of concepts like “Physical AI” and “compute economy” shows that AI is breaking out of the lab and into industrial workflows and monetization models that can be measured in utilization rates and ROI.

Investors inclined to buy the AI story via a narrow set of megacaps may come away from Computex with a more nuanced view. The upside case is that AI spending broadens across hardware, software, and services. The risk case is that profit pools fragment just as quickly.

The Sophisticated Investor’s Checklist

For those toggling between Taipei livestreams and earnings models, Computex 2026 offers a working checklist:

Watch how often companies talk about AI “factories” versus individual products; the more they sound like platforms, the more durable their narratives may be.

Pay attention to who is solving unglamorous problems—governance of compute, edge deployment, integration into legacy systems—rather than just showcasing glossy demos.

Track whether consumer‑facing brands can translate AI features into pricing and volume, not just marketing slogans.

In a market that has already rewarded anything with an AI ticker, Computex functions as both a hype filter and a discovery engine. The challenge for investors is not spotting the booths with the longest lines, but identifying which of these AI stories can survive a full cycle of rates, regulation, and reality.

The Sources

[1] NVIDIA GTC Taipei at COMPUTEX: Live Updates on … https://blogs.nvidia.com/blog/nvidia-gtc-taipei-computex-2026-news/ [2] COMPUTEX Taipei 2026 https://semiwiki.com/event/computex-taipei-2026/ [3] COMPUTEX 2026 Brings the Global AI Ecosystem to Taipei https://www.hpcwire.com/off-the-wire/computex-2026-brings-the-global-ai-ecosystem-to-taipei/ [4] COMPUTEX 2026 Brings the Global AI Ecosystem to Taipei https://www.prnewswire.com/news-releases/computex-2026-brings-the-global-ai-ecosystem-to-taipei-302702075.html [5] INFINITIX at COMPUTEX 2026: Turning AI Infrastructure … https://finance.yahoo.com/sectors/technology/articles/infinitix-computex-2026-turning-ai-020000153.html [6] COMPUTEX TAIPEI https://www.youtube.com/user/COMPUTEXtv [7] COMPUTEX Taipei https://www.nxp.com/company/about-nxp/events/computex-taipei:NXP-AT-COMPUTEX-TAIPEI [8] ADLINK Unleashes Physical AI at COMPUTEX 2026 https://www.adlinktech.com/en/news/adlink-computex-2026 [9] ASUS will present AI innovations at Computex 2026 … https://press.asus.com/news/press-releases/computex-2026-asus-rog-ai-gaming-innovation/ [10] Meet the ‘Corporate Bro’ Making Millions Satirizing Tech … https://www.wsj.com/business/media/meet-the-corporate-bro-making-millions-satirizing-tech-sales-dccaf132 [11] The Anti-Status Watch: Why Men in Finance Love Cheap … https://www.wsj.com/style/fashion/the-anti-status-watch-why-men-in-finance-love-cheap-cheesy-watches-d3c905fc

U.S. equities finished the week ending May 29, 2026 with major indices hovering near or at record highs, led again by large‑cap technology and AI beneficiaries, against a backdrop of easing inflation data and fragile but improving geopolitical sentiment. Bond yields drifted lower after April’s core PCE data came in slightly better than feared, helping financial conditions and supporting risk appetite even as the Federal Reserve keeps policy rates unchanged.

Index performance and leadership

The S&P 500 and Nasdaq spent the week grinding higher and closing around fresh records, with tech once again the main engine of gains as investors leaned into AI, semiconductors, and software. The Dow Jones Industrial Average lagged but still notched a modest advance, reflecting rotation away from some traditional cyclicals and toward high‑growth and quality secular winners.

Large‑cap tech strength was evident in the Nasdaq’s roughly 8% gain for May, underscoring how narrow leadership remains even as headline indices hit records. By contrast, small caps and more economically sensitive sectors showed a choppier pattern as markets weighed higher-for-longer real yields and uneven global growth.

Sector moves: tech, cyclicals, defensives

Technology outperformed broadly, with chipmakers and AI‑exposed hardware names benefiting from strong demand signals and positive news on high‑bandwidth memory and data‑center infrastructure. Software and cloud names also participated, with selective earnings beats and investment plans in hyperscale infrastructure helping sentiment in the broader growth complex.

More cyclical areas such as industrials and parts of consumer discretionary were mixed, constrained by still‑elevated long‑term rates and concerns that higher energy and input costs could pressure margins. Defensives like utilities and staples saw only modest interest as lower yields supported growth assets, although investors kept some ballast given geopolitical risks and an extended equity rally.

Rates, inflation, and Fed expectations

U.S. Treasury yields, which had pushed higher earlier in the year, eased during the week as April core PCE inflation came in slightly softer than markets feared, helping real yields edge down from recent highs. This “better‑than‑feared” inflation print reinforced expectations that while the Federal Reserve is in no rush to cut, the bar for renewed tightening remains high so long as disinflation continues gradually.

The Fed’s late‑April decision to hold the federal funds rate at 3.5% to 3.75% kept policy in a restrictive stance, but Chair Powell’s tone has emphasized data dependence rather than a preset path, leaving markets highly sensitive to each incremental inflation and labor‑market release. Implied rate‑cut expectations for late 2026 remain roughly intact, but the distribution of outcomes is wider, supporting demand for quality balance sheets and sustainable earnings growth over more speculative exposures.

Macroeconomic data and growth outlook

Macro data during the period painted a picture of an economy slowing from above‑trend levels but still avoiding a sharp downturn, consistent with a “soft landing with air pockets” narrative. Prior weeks’ data showed resilient consumer spending and tight but gradually cooling labor conditions, with retail sales and jobless claims pointing to deceleration rather than collapse.

At the global level, the IMF’s January World Economic Outlook update projected 2026 growth of about 3.3%, a slight upgrade that reflects improved prospects in several major economies but still well below pre‑pandemic norms. For markets, this combination of moderate global growth and easing inflation remains broadly supportive for risk assets, but it also heightens differentiation across regions and sectors as policy paths diverge.

Geopolitics, oil, and cross‑asset signals

Geopolitics again intersected with markets as headlines around U.S.–Iran tensions and cease‑fire negotiations influenced both equity and commodity price action. Reports late in the week that the parties were working toward a renewed 60‑day framework to extend the cease‑fire and begin nuclear talks helped support risk sentiment and contributed to a pullback in oil prices from overnight spikes.

Crude Oil, which had been volatile amid Middle East risks and supply worries, finished the broader period well off its recent highs at $87.89/bbl, with May on track for its largest monthly drop (17.79%) since 2020 despite not approaching the feared 200‑dollar‑per‑barrel scenario some had highlighted earlier in the year. Lower energy prices eased near‑term inflation anxiety and supported consumer‑oriented equities, even as energy producers and related cyclicals saw performance headwinds.

Global equities: Asia‑Pacific and Europe

Asia‑Pacific markets reflected both regional growth dynamics and the pull of Wall Street’s tech rally, with several indices hitting or approaching records despite intermittent risk‑off sessions around Middle East developments. South Korea’s Kospi surged more than 3% to a new intraday record before paring gains, buoyed in part by strength in key technology exporters.

Japan’s equity markets were more volatile, with the Nikkei and Topix swinging between pullbacks and new highs as investors balanced yen weakness, BOJ policy uncertainty, and strong corporate earnings. Elsewhere in the region, Australia’s S&P/ASX 200 advanced, while Chinese benchmarks were mixed, underscoring lingering concerns about China’s property sector and growth trajectory.

Credit, volatility, and market internals

Credit markets remained relatively calm, with spreads contained and little sign of systemic stress, consistent with the equity rally and improved risk sentiment. However, higher all‑in yields and the year‑to‑date backup in government bond rates continued to weigh on parts of the rate‑sensitive complex, including some REITs and leveraged cyclicals.

Equity volatility stayed subdued overall, but under the surface there was notable dispersion across sectors and factors, with AI‑linked names significantly outperforming more traditional areas such as homebuilders and retail. This internal divergence—strong index‑level returns, narrow leadership, and mixed breadth—remains a key theme for portfolio construction heading into June.

Positioning implications for investors

For diversified equity investors, the week reinforced a familiar message: staying invested in high‑quality growth and AI‑beneficiaries has been rewarded, but concentration risk is rising as a small group of leaders drives index performance. Many allocators are responding by pairing core large‑cap growth with selective exposure to cyclicals and value that can benefit if global growth and capex broaden beyond the current tech‑led cycle.

In multi‑asset portfolios, the combination of easing long‑term yields, moderating inflation, and a still‑restrictive Fed argues for balanced risk: maintaining equity exposure while using high‑quality bonds as both income generators and potential hedges if growth disappoints. With volatility low and geopolitical risks unresolved, options and other tail‑hedging tools remain under consideration as relatively inexpensive insurance against an abrupt regime shift.

VP Watchlist Updates

Below is an update‑style snapshot on the VP Watchlist names for the week, focused on recent catalysts, positioning, and narrative rather than precise price moves.

Astera Labs, Inc. (ALAB, $342.85, +15.11% over the last 5-days)

Astera Labs, Inc. (Nasdaq: ALAB), a leader in semiconductor-based connectivity solutions for rack-scale AI infrastructure, recently (May 5) announced preliminary financial results for the first quarter of fiscal year of 2026, ended March 31, 2026. they highlighted the following: Record quarterly revenue of $308.4 million, up 14% QoQ and up 93% year-over-year, Market-leading PCIe 6 AI fabric and signal conditioning portfolio delivered strong growth during Q1, & Now shipping newly announced Scorpio™ X-Series 320-lane AI Fabric switch and expanded Scorpio P-Series PCIe 6 switch family supporting 32 to 320 lanes.

Amwell® (AMWL, $9.83, +24.27% over the last 5-days)

Amwell announced (May 5) financial results for the first quarter ended Mar. 31, 2026.“Entering 2026, Amwell’s main focus was to consolidate our platform to fulfill the unmet needs of our Payer and Provider customers. The Technology-Enabled Care infrastructure we have developed to fill that gap in the market continues to gain traction as customers recognize its clear advantages: lower costs, better outcomes, stronger market share and an increased level of control and agility. Our platform is performing well and built to leverage the latest AI-powered innovations, positioning it as essential infrastructure for tech-enabled care delivery,” said Dr. Ido Schoenberg, Chairman and CEO of Amwell. “We are seeing powerful validation of the platform with significant pipeline growth and a number of meaningful renewals. With this momentum and the favorable regulatory tailwinds, Amwell is well-positioned for continued strong execution this year and to reach our goal of positive cash flow from operations in the fourth quarter.”

Eupraxia Pharmaceuticals (EPRX, $7.09, +2.09% over the last 5-days)

Eupraxia Pharmaceuticals Inc. (EPRX), a clinical-stage biotechnology company leveraging its proprietary Diffusphere™ technology designed to optimize local, controlled drug delivery for applications with significant unmet need, announced (May 5) the first Eosinophilic Esophagitis Endoscopic Reference Score (EREFS) data from its ongoing Phase 1b/2a part of the RESOLVE trial evaluating EP-104GI for the treatment of eosinophilic esophagitis (“EoE”). These data were also presented at the ongoing Digestive Disease Week (“DDW”) conference in Chicago. “The EREFS is an important, validated visual index of severity of EoE disease in the esophagus of patients. It measures edema, rings and strictures and other visible markers of disease often associated with symptoms. Today’s data demonstrated improvement in two key outcomes with EP-104GI in the treatment of EoE: first, that a full injection protocol of 20 injections resulted in more pronounced improvement than a protocol with fewer injections and less coverage area within the esophagus; second, with the higher number of injections, a consistent response in both the inflammatory and fibrotic sub scores of EREFS was observed,” said Dr. James A. Helliwell, Chief Executive Officer of Eupraxia. “This EREFS data being reported at DDW is consistent with the improvements we have seen in EoE symptoms and tissue health (EoEHSS) and suggests improvement in inflammation, fibrosis and the associated narrowing of the esophagus.”

Eurpraxia announced on Friday, May 1, the appointment of Dr. Jeymi Tambiah as Chief Medical Officer (CMO) as well as the retirement of Dr. Mark Kowalski, Eupraxia’s current CMO. Dr. Jeymi Tambiah (MB ChB, FRCS, MS, FAPCR, FFPM), is a Board Certified Cardiothoracic Surgeon physician scientist who practiced at Guys and St Thomas’ Hospitals prior to entering the biopharmaceutical industry in 2008. Dr. Tambiah brings over 18 years of experience in clinical development, medical and regulatory strategy, and product commercialization across pharmaceutical and biotechnology organizations.

Eupraxia recently co-hosted a Tribe Public www.TribePublic.com, CEO Presentation & Q&A Webinar event, Wednesday, April 1 titled “Turning EOE Into a Once-a-Year Appointment.” The event featured James A. Helliwell, M.D., Co‑founder and CEO of Eupraxia Pharmaceuticals (NASDAQ: EPRX), who discusses the company’s precision drug‑delivery platform, its approach to Eosinophilic Esophagitis (EoE), and broader pipeline priorities, followed by a focused 5–10 minute Q&A. You may watch it now at this Youtube link.

Modular Medical (MODD, $4.98, +20% over the last 5-days)

Modular Medical, Inc. (NASDAQ:MODD), a leader in innovative, patient-centric insulin delivery, saw (May 1) CEO Jeb Besser join Tribe Public’s members to unpack a simple question with big implications: what happens when an “almost‑pumper” market finally meets an FDA‑cleared device built for the rest of us, not just the superusers? Tribe Public hosted its CEO Presentation and Q&A Webinar, “From FDA Wins to Scaling Manufacturing – What Investors Should Watch,” on Friday, May 1, 2026, at 8:00 a.m. PT / 11:00 a.m. ET. In keeping with Tribe’s reputation for efficient programming, the session ran approximately 30 minutes, pairing a focused prepared talk with a 5–10 minute live Q&A segment that allowed investors to drill into timelines, capital needs, and commercial strategy. Besser’s formal remarks were framed under the title “From FDA Wins to Scaling Manufacturing – What Investors Should Watch,” setting the tone for a discussion that sat at the intersection of regulation, innovation, and recurring‑revenue hardware. By registering, attendees also joined Tribe Public’s membership base, ensuring they will receive future invitations to CEO briefings, sector spotlights, and investor wish‑list events.

Modular Medical announced (APRIL 19) the pricing of a registered direct offering consisting of 750,000 shares of the Company’s common stock at an offering price of $4.50 per share. The gross proceeds to the Company from the Offering are estimated to be approximately $3.4 million before deducting placement agent fees and other offering expenses. The Offering is expected to close on or about April 21, 2026, subject to the satisfaction of customary closing conditions.

Modular Medical’s latest regulatory milestone upgrades the narrative: the company has now (April 9) secured FDA 510(k) clearance for its Pivot tubeless insulin patch pump, moving from “launch‑ready” to “launch‑approved” in the heart of the fast‑growing diabesity market. The FDA has cleared Modular Medical’s Pivot patch pump as a tubeless, removable insulin delivery system, formally validating the device’s design and performance for commercial use in U.S. adults living with diabetes. The clearance converts what had been a Q1 2026 launch “subject to FDA response” into a tangible commercial pathway, giving the company permission to sell into an insulin pump market that has been estimated at roughly 8 billion dollars globally. Pivot is engineered as a simplified, two‑part patch pump with a 3‑milliliter removable reservoir, no need for battery recharging, and the ability to bolus without a dedicated controller, aiming squarely at patients who have stayed on multiple daily injections because traditional pumps felt too complex, cumbersome, or costly. By clearing Pivot, the FDA is effectively endorsing Modular Medical’s attempt to make advanced insulin delivery feel less like adopting a gadget and more like upgrading a daily habit.

The InterGroup Corporation (INTG, $38.76, +3.44% over the last 5-days )

The InterGroup Corporation (NASDAQ: INTG) announced financial (May 11) results for the fiscal third quarter ended March 31, 2026. InterGroup is a diversified holding company with interests in hospitality (through its majority‑owned subsidiary Portsmouth Square, Inc.), real estate operations, and investment transactions. The discussion below is derived from the Company’s Quarterly Report on Form 10‑Q for the quarter ended March 31, 2026. Third Quarter Fiscal 2026 Highlights (Three Months Ended March 31, 2026 vs. 2025) are as follows:

Total revenues increased to $20.372 million from $16.824 million (+21%).

Income from operations increased to $4.260 million from $2.350 million (+81%).

GAAP net income was $0.595 million, compared to a GAAP net loss of $0.750 million in the prior‑year quarter.

Net income attributable to InterGroup was $0.457 million, or $0.21 per diluted share, compared to a net loss attributable to InterGroup of $0.578 million, or $0.27 per share, in the prior‑year quarter.

Hotel revenues increased to $16.497 million from $12.210 million (+35%). For additional context, Hotel revenues for the quarter ended March 31, 2026 exceeded the comparable pre‑pandemic quarter ended March 31, 2019 by approximately $1.028 million.

Real estate revenues were $3.875 million compared to $4.614 million in the prior‑year quarter (‑16%).

Net loss from investment transactions was $(0.342) million compared to $(1.379) million in the prior‑year quarter.

Volato Group, Inc. (SOAR) & M2i Global, Inc. (MTWO, +11.76% over the last 5-days)

Nokia has quietly stitched together a new chapter in its comeback story—one that runs from American living rooms to Pentagon test ranges, and now straight through NVIDIA’s (NVDA) data centers. With NVIDIA’s billion‑dollar vote of confidence in the fall and another blockbuster NVIDIA earnings report due today, the old handset icon is suddenly speaking fluent AI.

Nokia announced (May 21) the launch of its AI Networking Innovation Lab, a new center designed to drive co-innovation with AI and cloud partners and accelerate the development of next-generation networking technologies for artificial intelligence (AI) infrastructure. Located within Nokia’s Sunnyvale, California facility, the lab serves as an innovation hub where Nokia will work across advanced AI networking technologies, architectures and ecosystems with a variety of partners to help shape the future of data center networking. AI workloads are fundamentally changing how data center networks must operate. The performance, scale, and precision required to support large-scale AI training and distributed, real-time inference place unprecedented demands on networking infrastructure. To address these challenges, Nokia is adopting a new approach to how technologies are integrated, tested, and deployed from the ground up for the AI era.

Nvidia’s First Quarter Fiscal 2027 earnings report crossed the tape Wednesday, May 20, and the immediate takeaway is that the AI engine is still running at full throttle, even if Wall Street was already leaning hard on the accelerator. The story today is less about whether Nvidia is growing and more about just how far into “infrastructure of AI” territory it has now ventured.

McDonald’s (MCD, $279.20)

Morgan Stanley (April 21) has adjusted its price target on McDonald’s (MCD) to $334, maintaining an Equal Weight stance on the stock. The firm’s analyst highlighted consumer strength heading into first-quarter results, noting that earnings quality will likely vary across the restaurant and food distribution landscape . While some operators may face headwinds, the underlying consumer backdrop remains robust, which could support McDonald’s performance as one of the industry’s quality players positioned to navigate the current environment .

Tesla (TSLA, $435.79, +4.29% over the last 5-days)

Tesla’s Q1 2026 performance underscored strong revenue growth and signs of margin stabilization, supported by continued investment in solar and AI initiatives. The narrative is further bolstered by Tesla’s stake in SpaceX, with anticipation building around a potential SpaceX IPO that could unlock additional shareholder value soon. However, elevated capital expenditure levels remain a key overhang, tempering investor enthusiasm despite these strategic advantages.

Serina Therapeutics (NYSE: SER, $1.84)

Serina Therapeutics, Inc. (“Serina” or the “Company”) (NYSE American: SER), a clinical-stage biotechnology company developing its proprietary POZ Platform™ drug optimization technology, reported (May 14) its financial results for the first quarter ended March 31, 2026, along with key business updates. The company highlighted the follow: Phase 1b Registrational Clinical Study of SER-252 Underway in Advanced Parkinson’s Disease; TFL data from the SAD study arm targeted for first half of 2027 & Closed $21.2 million private placement financing to support continued advancement of SER-252. “With our Phase 1b registrational study of SER-252 now underway and a strengthened balance sheet, Serina is entering an important execution phase as we work toward our first clinical data in patients with advanced Parkinson’s disease,” said Steve Ledger, Chief Executive Officer of Serina. “SER-252 represents the first clinical validation of our POZ Platform™, which is designed to optimize well-understood therapeutics by improving pharmacokinetics, tolerability and dosing profiles. We believe this approach has the potential to unlock meaningful value across multiple modalities, and we are building a pipeline and partnership strategy to fully leverage the breadth of the platform.”

BuzzFeed, Inc. (BZFD, $1.63)

BuzzFeed, Inc. (“BuzzFeed” or the “Company”) (Nasdaq: BZFD) today announced the closing of its previously announced transaction with Allen Family Digital, LLC, an affiliate of Byron Allen’s Family Office, under which Allen Family Digital, LLC acquired approximately 51% of the Company’s outstanding shares. Byron Allen has assumed the role of Chairman and Chief Executive Officer, and Jonah Peretti has transitioned to his newly created role as President of BuzzFeed AI. Under the terms of the agreement, Allen Family Digital acquired 40 million shares of BuzzFeed, Inc. common stock at a price of $3.00 per share, representing a total transaction value of $120 million for a total purchase price of $120 million. The transaction was funded with $20 million in cash at closing and a $100 million promissory note due five years from closing, accruing interest at 5% annually. BuzzFeed has used $12.5 million of the cash proceeds from the transaction to pay down existing indebtedness, materially strengthening the Company’s balance sheet and enhancing financial flexibility to support future growth initiatives. “Jonah is a great visionary and has done a phenomenal job. BuzzFeed and HuffPost have become two iconic global digital media brands with powerful audience reach and strong cultural importance,” said Byron Allen, Chairman and CEO of BuzzFeed. “Our vision is to build on the iconic foundation of BuzzFeed and HuffPost by expanding into free-streaming video, audio and user-generated content. As of this moment, with the power of AI, BuzzFeed is officially chasing YouTube to become another premier free-streaming video service.”

FMC Corporation (NYSE: FMC, $13.66, +5% over the last 5-days)

FMC Corporation (NYSE:FMC) reported (April 29) first quarter 2026 results above guidance with Adjusted EBITDA above high end of range, reaffirms full-year outlook. Their first quarter 2026 revenue of $759 million, down 4 percent versus first quarter 2025. First quarter 2026 revenue, excluding India, was $762 million, down 4 percent versus first quarter 2025, which included India. On a GAAP basis, the company reported a loss of $2.25 per diluted share in the first quarter, a decrease of $2.13 versus first quarter 2025. First quarter adjusted loss per diluted share of $0.23 was down 41 cents versus first quarter 2025. FMC Corporation also announced today that its board of directors declared a regular quarterly dividend of 8 cents per share (roughly 2.26%), payable on July 16, 2026, to shareholders of record as of the close of business on June 30, 2026.

GeoVax Labs, Inc. (GOVX, $2.06)

GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing immunotherapies and vaccines, announced (May 26) a strategic prioritization of its development portfolio to concentrate resources on its lead programs, GEO-MVA and Gedeptin(R), reflecting increasing clinical, regulatory, and market alignment across these programs. As part of this decision, the Company has elected to discontinue active development activities related to its GEO-CM04S1 COVID-19 vaccine candidate. This decision was not related to any safety concerns with the vaccine but reflects the continued evolution and contraction of the global COVID-19 vaccine market, and GeoVax’s focus on programs with clearer regulatory pathways, stronger demand visibility, and more immediate commercialization potential. GeoVax emphasized that portfolio prioritization is a standard and essential practice within the biotechnology industry, enabling companies to align resources with the highest-value opportunities as market conditions and scientific landscapes evolve.

Tribe Public’s CEO Presentation and Q&A Webinar Event titled “Ebola, Marburg, Hantavirus, Mpox and Beyond: Building a Resilient Infectious Disease Portfolio Preparedness Strategy” was held Thursday, May 28, 2026. David Dodd, Chairman and Chief Executive Officer of GeoVax Labs, Inc. (NASDAQ: GOVX) delivered a presentation titled “Ebola, Marburg, Hantavirus, Mpox and Beyond: Building a Resilient Infectious Disease Portfolio Preparedness Strategy” and was available for a Q&A session.

Dell Technologies (DELL, $420.91, +66.50% over the last 5-days)

Dell Technologies spent its first fiscal quarter of 2027 rewriting its own growth narrative. The company posted record revenue of about $43.8 billion, an 88% year‑over‑year surge that marked its fastest top‑line expansion since it returned to public markets in 2018 and blew past analyst projections on both sales and earnings. The market response was anything but modest: Dell’s shares jumped more than 30% in after‑hours trading as investors rushed to reprice a company that had been treated as a mature PC and enterprise name into something closer to an infrastructure‑for‑AI story. Record diluted EPS—north of $5 per share on a GAAP basis and nearly $4.90 on a non‑GAAP basis—combined with more than $4 billion in operating cash flow to give the quarter just enough superlatives to justify the rally.

The Sources

[1] Stocks close at record highs with tech leading the way again. Nasdaq gains 8% in May https://www.cnbc.com/2026/05/28/stock-market-today-live-updates.html [2] NYSE: The New York Stock Exchange https://www.nyse.com/index [3] FOMC Introductory Statement, April 29, 2026 https://www.youtube.com/watch?v=jRgIxhMZF2E [4] S&P 500 and Nasdaq close at new records, lifted by tech rally: Live updates https://www.cnbc.com/2026/05/27/stock-market-today-live-updates.html [5] Stock Market News for May 29, 2026 https://www.theglobeandmail.com/investing/markets/stocks/LLY/pressreleases/2201759/stock-market-news-for-may-29-2026/ [6] Weekly Market Recap https://www.jhinvestments.com/weekly-market-recap [7] Weekly Market Recap https://am.jpmorgan.com/content/dam/jpm-am-aem/americas/us/en/insights/market-insights/wmr/weekly_market_recap.pdf [8] 2026 Market Outlook | J.P. Morgan Global Research https://www.jpmorgan.com/insights/global-research/outlook/market-outlook [9] Stock market news for May 14, 2026 https://www.cnbc.com/2026/05/13/stock-market-today-live-updates.html [10] World Economic Outlook Update, January 2026 https://www.imf.org/en/publications/weo/issues/2026/01/19/world-economic-outlook-update-january-2026 [11] US Markets, Company Earnings, Stock Market Trends … https://www.morningstar.com/markets [12] Fri, May 29, 2026 🇺🇸 US Post-Market — Looking ahead, all eyes are on next https://www.youtube.com/watch?v=2c5UsZc9LlM [13] Dell Results, Peace Talks Provide Small Early Lift https://www.schwab.com/learn/story/stock-market-update-open [14] Stock Market Updates Live: आज कहां करें इन्वेस्ट | Business … https://www.youtube.com/watch?v=XK0-Puxddn0 [15] Market Recap – May 29, 2026 #MarketRecap … https://www.facebook.com/sarmaayapk/posts/market-recap-may-29-2026marketrecap-kse100index-sarmaayafinancial/1571467361655554/

Ford Motor Company’s (F) latest pivot has Wall Street cheering and value investors double-checking the ticker to make sure this really is Ford and not a rebranded AI infrastructure play in disguise. The 122‑year‑old automaker is turning EV growing pains into a grid‑scale energy storage story that suddenly makes the “old economy” look like a clever derivative trade on the AI data‑center boom.

Ford: From Driveways To Data Centers

Ford Motor Company’s new Ford Energy subsidiary marks a deliberate step beyond selling F‑150s and Mustangs into selling megawatt‑hours to utilities, data‑center operators, and industrial customers. Management plans to invest roughly 2 billion dollars and repurpose U.S. EV battery capacity, including a Kentucky plant, to build large‑scale battery energy storage systems rather than just more electric SUVs that consumers are hesitating to buy.

In practice, that means Ford is redirecting battery expertise from driveways to data centers, aiming for at least 20 gigawatt‑hours of annual storage capacity with first systems expected to ship around 2027–2028. For investors, it reframes Ford as a potential infrastructure supplier to the AI era rather than a pure EV demand call.

Why Ford Stock Is Suddenly “Hot”

Ford’s stock has surged in recent weeks as the market digests the Ford Energy announcement and its implications. Shares jumped more than 20% over two days following the launch of the subsidiary, with some sessions showing single‑day gains in the high single digits as investors embraced the narrative shift.

This isn’t enthusiasm for yet another crossover launch; it’s a rerating based on Ford potentially supplying batteries to power‑hungry AI and cloud data centers. One might say the stock is finally getting credit not just for how fast it can go from zero to sixty, but for how long it can keep a server farm online when the grid starts to sweat.

The Ford Energy Game Plan

Ford Energy is structured as a wholly owned subsidiary that will manufacture and sell U.S.‑assembled battery energy storage systems for utilities, large industrial users, and hyperscale data‑center operators. The company is targeting grid‑scale units of at least 5 megawatt‑hours each, leaning on lithium iron phosphate (LFP) chemistry and using repurposed EV battery facilities to accelerate deployment while containing capital intensity.

Executives have outlined a ramp to at least 20 gigawatt‑hours of capacity per year, with deliveries of storage systems slated to begin in the late 2020s. It’s an industrial strategy with a twist: Ford is effectively writing off tens of billions in EV bets while committing a couple of billion to a business where demand is growing, power prices are volatile, and customers tend to sign multi‑year contracts rather than haggle over leather seats.

First Customer: EDF, And A Grid‑Scale Debut

Ford Energy’s story moved from press release to purchase order when the unit signed its first framework agreement with EDF power solutions North America, a subsidiary tied to French energy major Électricité de France (EDF.PA). Under the five‑year agreement, EDF can procure up to 4 gigawatt‑hours of Ford Energy storage systems annually, for a total potential volume of 20 gigawatt‑hours over the life of the deal, with deliveries expected to begin in 2028.

The EDF contract gives Ford something more valuable than a great investor slide: external validation that a global energy player is willing to underwrite its grid‑storage ambitions at scale. Wall Street’s initial reaction to the EDF deal itself was muted compared with the earlier announcement spike, but the commercial progress supports the idea that Ford Energy is not just a headline‑driven meme trade.

Riding The AI And Data‑Center Power Wave

The strategic backdrop is straightforward: AI workloads and cloud computing are driving a surge in electricity demand and grid‑stability challenges, and investors are hunting for ways to play that theme beyond the usual semiconductor and hyperscaler suspects. Ford now aims to be one of the companies selling the literal batteries that keep those GPU clusters humming when the grid gets cranky.

In essence, Ford is positioning itself as an infrastructure vendor to the likes of major cloud platforms and data‑center operators, complementing a broader ecosystem that includes AI chip makers such as NVIDIA (NVDA), power‑gear specialists like Eaton (ETN), and renewable developers worldwide. The key twist—and source of investor intrigue—is that Ford is leveraging manufacturing scale, existing plants, and supply‑chain relationships to chase a market that looks more like long‑cycle industrials and energy infrastructure than cyclical consumer autos.

Rewiring The EV Narrative

Ford’s pivot into storage partly reflects the humbling reality of EV adoption curves and capital deployment. The company has effectively acknowledged that some of its EV investments will not earn their originally hoped‑for returns, reportedly writing off a large chunk of prior spending while carving out a 2 billion dollar commitment to the grid‑scale storage business.

Instead of doubling down on a crowded EV market, Ford is taking battery expertise and manufacturing real estate and applying them to a segment where its scale and industrial roots are genuine advantages. Investors inclined to see every EV adjustment as a confession of defeat might need to update their models: this is less “EV retreat” and more “battery redeployment” into a power market now being reshaped by AI, renewables, and electrification.

What This Could Mean For Investors

For shareholders in Ford (F), the Ford Energy initiative introduces an option‑like upside tied to long‑term secular growth in energy storage demand. If Ford executes on its 20 gigawatt‑hour annual capacity target and continues to land multi‑year deals with utilities, data centers, and industrial customers, the business could evolve into a meaningful earnings contributor that is less cyclical than vehicle sales and less dependent on consumer sentiment.

At the same time, investors should remember that grid‑scale storage is capital intensive, competitive, and technologically dynamic, with players ranging from battery specialists to independent power producers and renewables developers. Ford’s advantage lies in its manufacturing muscle, U.S.‑based assembly footprint, and ability to pivot an existing supply chain into a market that is rapidly moving from pilot projects to multi‑gigawatt‑hour procurement.

The Punchline: An Old Icon With A New Hook

Ford’s story now offers a rare mix in today’s market: a century‑old brand, a beaten‑up legacy auto multiple, and a newly emerging claim on one of the most sought‑after themes in equities—powering the AI revolution. The stock has responded as investors re‑rate the company not just as a cyclical carmaker, but as a potential supplier of critical infrastructure to the digital economy’s new factory floor: hyperscale data centers.

In a market where valuations often assume every growth story must arrive wrapped in a cloud‑software logo, Ford is attempting something slightly subversive—using metal, factories, and battery chemistry to turn yesterday’s EV headaches into tomorrow’s grid‑storage cash flows. For investors, it may be time to refresh the watchlist: the ticker is still F, but the narrative now reads “Ford Motor, powered by kilowatt‑hours and GPUs.”

The Sources

Ford stock is powering up as the automaker dives into energy storage – Yahoo Finance https://ca.finance.yahoo.com/news/ford-stock-is-on-fire-as-it-dives-into-energy-storage-131029427.html[ca.finance.yahoo]

Ford’s stock is surging—and it’s got nothing to do with its pickup trucks – The Wall Street Journal https://www.wsj.com/finance/stocks/ford-stock-rise-why-4f1c632a[wsj]

Ford stock surges as energy storage ambitions fuel investor optimism – CBT News https://www.cbtnews.com/ford-stock-investor-optimism-energy-storage/[cbtnews]

Ford launches energy storage business with plans for U.S.-assembled systems – CBT News https://www.cbtnews.com/ford-launches-energy-storage-business/[cbtnews]

Ford’s 2 billion dollar pivot into grid batteries signals a new chapter – Yahoo Finance / Energy sector https://finance.yahoo.com/sectors/energy/articles/ford-2b-pivot-grid-batteries-104000902.html[finance.yahoo]

Ford stock is hot as automaker jumps into AI data center energy boom – Bloomberg https://www.bloomberg.com/news/newsletters/2026-05-21/ford-stock-is-hot-as-automaker-jumps-into-ai-data-center-energy-boom[bloomberg]

Ford Energy lands its first customer in battery storage deal – Detroit Free Press https://www.freep.com/story/money/cars/ford/2026/05/18/ford-battery-energy-storage-systems-edf-deal/90140790007/[freep]

Ford launches “Ford Energy” for grid-scale BESS – Automotive Manufacturing Solutions https://www.automotivemanufacturingsolutions.com/electrification/ford-launches-ford-energy-for-gridscale-bess/2662378[automotivemanufacturingsolutions]

ESG Today: Ford repurposes EV battery capacity to launch new energy storage business https://www.esgtoday.com/ford-repurposes-ev-battery-capacity-to-launch-new-energy-storage-business/[esgtoday]

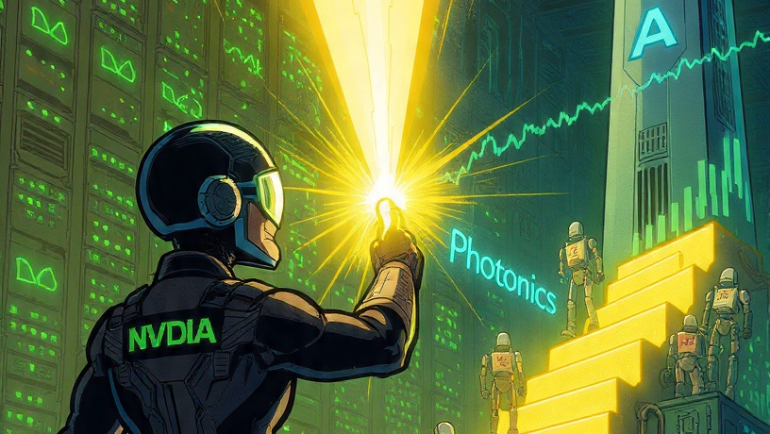

Nvidia’s latest photonics splurge reads less like a tech news item and more like a capital-markets rom‑com: a dominant chipmaker buying the lasers, the networks, and even a telecom co‑star to make sure the AI boom doesn’t run out of bandwidth.

Nvidia Buys the Light Bulbs for the AI Gold Rush

In the classic gold rush, it was the shovel sellers who retired early; in the AI rush, Nvidia (NVDA) is determined to own the digital equivalent of the shovels, the railroads, and now, the fiber itself. The company has committed a combined 4 billion dollars to photonics specialists Coherent (COHR) and Lumentum (LITE), locking in critical optical components that shuttle data between its high‑end GPUs at blistering speeds.

By writing multibillion‑dollar purchase commitments into long‑term supply deals, Nvidia is effectively pre‑paying tomorrow’s bandwidth bill today—and sending a polite but firm message to the rest of the ecosystem: if you want to power large‑scale AI, you’ll be doing it on rails Nvidia helped lay down.

Coherent and Lumentum: From Niche Suppliers to Strategic Actors

For years, Coherent (COHR) and Lumentum (LITE) were the kind of names that only optical engineers, niche hedge funds, and the occasional trivia‑obsessed PM could casually drop into conversation. Nvidia’s 2‑billion‑dollar equity‑style injections into each outfit instantly upgraded them to front‑row roles in the next generation of AI infrastructure, with agreements covering advanced lasers, optical networking gear, and future capacity rights in new U.S. fabs.

The market noticed: on announcement, Lumentum shares jumped nearly 12%, while Coherent rallied about 15%, a reminder that in AI infrastructure, even a supplier can trade like a story stock when Nvidia appears on the cap table. Nvidia’s own shares added roughly 3%, suggesting investors are comfortable with the company behaving less like a chip vendor and more like a strategic holding company for the AI hardware stack.

Why Photonics Became a Strategic Obsession

At hyperscale, electrons are starting to feel a bit… 20th century. Shifting more interconnect from electrical to optical—swapping copper traces for photonics—promises higher bandwidth, lower latency, and better energy efficiency, all of which translate into more AI tokens per watt and more revenue per square foot of data center.

For Nvidia, photonics is not a side quest; it is the enabling technology that lets its next‑gen platforms—from current AI accelerators to forthcoming architectures like Vera Rubin—scale without turning data centers into small suns. The company’s multiyear agreements with Lumentum (LITE) and Coherent (COHR) explicitly tie investment dollars to access rights for the most advanced optical components, effectively ring‑fencing a portion of future innovation for Nvidia’s own AI road map.

The Nokia Angle: Teaching Old Networks New AI Tricks

If photonics is the bloodstream of AI infrastructure, wireless networks are its roaming nervous system—and Nvidia is quietly wiring those, too. In late 2025, Nokia (NOK) disclosed that Nvidia would take a 1‑billion‑dollar equity stake via newly issued shares, giving the chipmaker roughly 2.9% of the Finnish telecom equipment provider. Nokia stock promptly jumped more than 20% on the announcement and has since more than doubled as the partnership has taken shape.

The deal is more than a financial footnote: Nvidia (NVDA) and Nokia (NOK) are co‑developing AI‑powered radio access networks (AI‑RAN) and 6G‑ready infrastructure, targeting what they see as a 200‑billion‑dollar AI‑telecom market by 2030. Nokia is adapting its AirScale baseband systems to integrate Nvidia’s CUDA‑accelerated platforms and new AI‑centric RAN computers, effectively turning cell towers into edge AI appliances.

From Chips to an AI Infrastructure Conglomerate

Step back from the ticker tape and Nvidia (NVDA) increasingly looks less like a semiconductor company and more like a vertically insinuated AI infrastructure conglomerate. On one flank, it is anchoring the optics supply chain with Coherent (COHR) and Lumentum (LITE); on another, it is embedding itself into the future of mobile and fixed networks via Nokia (NOK).

The strategy has a familiar Wall Street ring: in the age of AI, control the inputs that scarce compute depends on—bandwidth, interconnect, and network intelligence—and you not only sell more chips, you influence the tempo of everyone else’s road map. For investors, the result is a company whose upside is tied not just to unit volumes of GPUs, but to the entire capex cycle of AI data centers and AI‑native networks.

Sophisticated Risk, But Not a Blind Bet

None of this is risk‑free, of course, and the market is sober enough to remember that vertical ambitions can overreach. Nvidia (NVDA) is now exposed not just to semiconductor cycles but also to swings in optical demand, telecoms capex, and the politics of industrial policy around U.S. manufacturing and 6G standard‑setting..

Yet the structure of these deals—nonexclusive agreements, purchase commitments tied to future capacity, and minority equity stakes in Nokia (NOK) rather than full acquisitions—suggests Nvidia is accumulating leverage, not fixed assets. It is, in effect, renting optionality on several high‑conviction themes: photonics, AI‑native networking, and 6G, while preserving the capital‑light profile that Wall Street has rewarded so generously.

The Investor Hook: A New AI Value Chain to Underwrite

For investors trying to position portfolios for the next phase of AI, this evolving map offers several concentric circles of exposure.

At the core sits Nvidia (NVDA), whose strategy increasingly resembles an AI‑era utility: it sells the compute, steers the road map, and now helps underwrite the optical and network layers the ecosystem depends on.

In the optical ring, Coherent (COHR) and Lumentum (LITE) gain visibility and validation as long‑term suppliers into Nvidia’s AI platforms, with potential spillover to other hyperscalers once capacity ramps.

On the network perimeter, Nokia (NOK) becomes a leveraged play on AI‑infused 5G‑to‑6G migration and AI‑RAN, benefiting from both Nvidia’s capital and its software ecosystem.

For now, the market seems content with the idea that the AI story is, if anything, “underhyped,” as some veteran investors have recently argued. Nvidia’s push into photonics and Nokia’s networks adds a new twist to that narrative: the AI trade is no longer just about who trains the models, but who owns the light and the air through which those models speak.

Nvidia to invest 4 billion dollars into photonics companies Coherent and Lumentum – CNBC https://www.cnbc.com/2026/03/02/nvidia-investment-coherent-lumentum.html[cnbc]

Nvidia announces strategic partnership with Lumentum to develop state‑of‑the‑art optics technology – Nvidia newsroom https://nvidianews.nvidia.com/news/nvidia-announces-strategic-partnership-with-lumentum-to-develop-state-of-the-art-optics-technology-for-ai[nvidianews.nvidia]

Nvidia announces 4‑billion‑dollar investment in Coherent and Lumentum – Photonics Media https://www.photonics.com/Videos/NVIDIA-announces-4-Billion-Investment-in/v1087[photonics]

Nokia’s board resolved on directed share issuance to Nvidia, 1‑billion‑dollar equity investment – Nokia https://www.nokia.com/newsroom/inside-information-nvidia-to-make-usd-1-billion-equity-investment-in-nokia-in-addition-to-new-strategic-collaboration/[nokia]

Nvidia takes 1‑billion‑dollar stake in Nokia, shares jump on AI‑RAN partnership – CNBC https://www.cnbc.com/2025/10/28/nvidia-nokia-ai.html[cnbc]

Commentary on Nvidia’s stake in Nokia and portfolio allocation – Stocks to Earn (Facebook post) https://www.facebook.com/Stockstoearnpage/posts/nvidia-is-holding-roughly-8-of-its-investment-portfolio-in-nokia-nok-following-a/[facebook]

Nvidia’s big investment in photonics while prepping Vera Rubin chips – Forbes https://www.forbes.com/sites/johnwerner/2026/03/11/nvidias-big-investment-in-photonics-while-prepping-vera-rubin-chips/[forbes]

Nvidia invests 4 billion dollars in photonics firms to boost AI chips – LinkedIn News brief https://www.linkedin.com/news/story/nvidia-invests-4b-in-photonics-firms-to-boost-ai-chips-7057732/[linkedin]

Veteran VC perspective: AI revolution is “underhyped” – Wall Street Journal https://www.wsj.com/tech/ai/john-doerr-ai-opinion-1d64ee60[wsj]

On a Friday when the S&P 500 idled, value and momentum briefly wore the same face: the top‑5 gainers—Dell (DELL), Okta (OKTA), NetApp (NTAP), Atlassian (TEAM), and ServiceNow (NOW)—didn’t just ride the market; they rewrote the narrative for high‑margin tech hardware and “boring” infrastructure with a dash of AI‑themed optimism.

A Friday Flirtation with Hyper‑Efficiency

By the close on May 29, 2026, the tape read like a mixing desk turned up too high on data‑centric stocks: Dell jumped roughly 35%, NetApp by more than 30%, Okta by over 20%, while Atlassian and ServiceNow tagged along as understated heavy‑lifters of the day’s momentum. For once, the crowd wasn’t chasing meme coins or space lasers; it was double‑clicking on companies that move, secure, and manage data at industrial scale.

Wall Street’s tone on the day bordered on giddy: computer‑hardware names suddenly looked less like legacy relics and more like “AI‑adjacent” infrastructure with pricing power. As one strategist put it dryly, “They’re not selling pizzas, they’re selling the ovens that bake the AI boom.”

DELL: The Elephant in the Room Gets a Raise

Dell’s surge owed partly to its latest quarter, which sailed past consensus on both revenue and adjusted EPS, with management hiking its full‑year EPS target to around $17.90 and guiding for roughly $165–$169 billion in revenue—well above prior Street estimates. That kind of delta between plan and reality is rarer in mature hardware than a bug‑free software release.

Investors seized the chance to reprice Dell as more than a PC‑maker: it’s now a portfolio of high‑margin server, storage, and infrastructure solutions that are quietly feeding every hyperscaler and federal‑cloud contract in sight. The stock’s one‑day spike, then, felt less like a short‑squeeze and more like a long‑overdue admission that Dell’s an “AI‑tethered” play, without the haircut typically associated with bleeding‑edge startups.

NTAP: NetApp Reboots the Value Playbook

NetApp, up in the low‑thirties in percentage terms, managed the impressive feat of looking like both a “value” pick and a growth‑adjacent infrastructure name on the same day. Its fiscal‑Q4 results and updated guidance beat expectations on adjusted earnings, revenue, and operating income, giving the market a rare triple‑confirm that NetApp’s data‑fabric and hybrid‑cloud strategy isn’t just PowerPoint.

The humor here is in the reversal: for years, NetApp was the “old‑school” data‑storage vendor traders joked about in the same breath as fax machines; today, the joke is on the shorts who still think efficiency‑focused data‑infrastructure is passé. With AI‑driven workloads demanding faster, smarter data pipelines, NetApp suddenly looked like the bartender at the AI party: unseen, essential, and quietly getting paid.

OKTA: Identity Management Gets a Identity Crisis in the Best Way

Okta’s 20‑plus percent jump was fueled by a revenue and profitability beat that outpaced expectations, along with guidance that nudged its full‑year targets higher. In the world of identity‑and‑access management, that’s the equivalent of a security firm not just locking the doors but handing the board a report that says the building is now more secure than the bank down the street.

What resonated with investors was the durability of Okta’s recurring revenue base and its expanding role as the “front‑door” to enterprise SaaS stacks. As companies obsess over ransomware, zero‑trust, and regulatory compliance, Okta’s rally served as a reminder that authentication is no longer a back‑office nicety; it’s a five‑alarm‑level profit center priced in dollars per seat.

TEAM & NOW: The Silent Engines of Productivity

Atlassian (TEAM) and ServiceNow (NOW) didn’t light the tape quite as explosively as DELL or NTAP, but they provided the steadying bass line to the day’s tech‑gainer symphony. TEAM and NOW both trade in productivity software that turns chaotic workflows into trackable tickets, sprints, and dashboards—work that pays better when the economy is running hot.

ServiceNow’s professional‑services and workflow‑automation platform, for instance, benefits every time a CFO decides that “we need to automate approvals” instead of “we need to hire more people.” Atlassian, meanwhile, keeps monetizing the realization that knowledge workers would rather juggle Jira, Confluence, and Bitbucket than a dozen disconnected spreadsheets.

The subtle bullish cue for investors: when even the “background” productivity names edge higher on a light‑news day, the market is saying demand for enterprise software is quietly, stubbornly robust.

Why This Gainer Pool Attracts Investors

The shared thread across DELL, OKTA, NTAP, TEAM, and NOW is that each is a high‑quality, recurring‑revenue‑leaning franchise with a tangible role in the AI‑driven infrastructure stack. They’re not the shiniest satellites, but they’re the rails, the locks, and the ticketing systems that keep the trains running.

For a company that’s built on the thesis that “identity is the new perimeter,” Okta Inc. (NASDAQ: OKTA) seems to be having a particularly good run. Over the past nine months, the last 10 press releases—from earnings beats to AI‑agent roadmaps—paint a consistent picture: a disciplined, cash‑generating identity platform that’s strategically repositioning itself for the agentic AI era.

Analysts love predictable growth; Wall Street swoons when that growth is paired with a clear secular tailwind. Okta is now delivering both—just with fewer PowerPoint slides and more concrete financials.

The Financial Backdrop: Steady, Profitable Growth

Start with the macros: in early March 2026, Okta reported its fourth quarter and full‑year fiscal 2026 results, logging total revenue of about $2.92 billion, up roughly 12% year‑over‑year, with subscription revenue growing at a similar clip. Fourth‑quarter revenue hit about $761 million, up 11% year‑over‑year, and GAAP operating income turned positive for the year, signaling a move beyond the “high‑growth, high‑burn” persona of prior cycles.

For the long‑term investor, the real signal is in the backlog: remaining performance obligations (RPO) and current RPO are both climbing double‑digits, implying that the growth run‑rate is not just real but contracted. That’s the kind of funding‑round‑like visibility that gives public‑market investors a warm glow without the liquidation preferences.

Management Cadence: Less Hype, More Guidance

The earnings‑related releases are bookended by a steady drumbeat of management‑roadshow and disclosure announcements. Okta flagged its Q4 FY26 results date in late January, then reiterated its first‑quarter FY2027 print date in May, with the FY27 outlook penciling in roughly 9% revenue growth and a sharply elevated non‑GAAP operating‑income and free‑cash‑flow corridor.

For the investor who dislikes earnings surprises, this is almost boring in the best sense: clear disclosure calendar, consistent cadence, and a “prudent but confident” tone that markets seem to reward. When a company shifts from “we’re figuring it out” to “here’s the playbook” in its press releases, it tends to trade like a platform company, not a speculative tech startup.

Industry Validation: From Analysts to Forrester

Validation from the ecosystem matters, and Okta’s recent press releases carry that subtext. In May 2026, the company announced that it was named a “Leader” in The 2026 Forrester Wave™: Workforce Identity Security Platforms, a nod that doesn’t move the stock in a single day but quietly reassures boards and procurement teams wrestling with vendor selection.

For the investor, this kind of third‑party framing is cheap optionality: it’s not a new contract, but it derisks the “who wins identity?” question in Okta’s favor. In a crowded category, being the default “Leader” on a Forrester grid is like being the safe‑harbor choice in a security committee meeting—especially when the committee is under pressure.

The AI Agent Story: From Buzzword to Blueprint

Okta’s most recent narrative pivot arrived in April 2026, when the company announced a “blueprint for the secure agentic enterprise” and the general availability of Okta for AI Agents. The press release leans into three questions that matter to any CISO: where agents are, what they can connect to, and what they can actually do.

The platform’s capabilities—discovery and registration of shadow agents, universal directory treatment of non‑human identities, an Agent Gateway to control access, and a “universal logout” kill switch—read like a security buyer’s checklist turned into product. To investors, this is code for “Okta is monetizing the AI‑agent layer before AI‑agent fatigue sets in.” It’s a subtle but important pivot: from being the identity layer for humans to being the identity layer for AI.

The Venture Angle: Investing in the Identity Ecosystem

Adding a second layer of narrative, Okta Ventures (the company’s investment arm) unveiled its 2026 “The Identity 25” report, spotlighting 25 companies shaping digital identity in the age of AI. The list spans agentic‑AI authentication, deep‑fake countermeasures, biometric security, passwordless approaches, and public‑digital‑identity projects, all of which sit comfortably within Okta’s broader “identity‑as‑infrastructure” thesis.

For investors, this is more than a PR exercise: it’s a signal that the company is deliberately curating the adjacent ecosystem around its core platform. Think of it as identity‑adjacent venture capital with a built‑in distribution channel—because those portfolio companies have a natural path to being integrated into Okta workflows.

Strategic Partnerships: From Golf Pros to Enterprise Automation

Recent releases also spotlight a few high‑signal partnerships. Okta deepened its relationship with the PGA of America to unify identity management for more than 30,000 golf professionals and employees, a move that looks modest until you realize it’s a test case for large‑scale, federated identity in a complex ecosystem.

On the enterprise‑automation front, Okta is collaborating with Automation Anywhere, Cisco, NVIDIA, and OpenAI on EnterpriseClaw, a capability designed to run claw‑style AI agents across cloud, desktop, on‑prem, and secure enterprise systems. For the investor, this is the “strategic partnership” box checked: Okta is not just a security vendor, but a plumbing layer embedded in others’ AI‑workflow stacks.

Why the Story Matters to Investors

Put together, the last 10 Okta press releases tell a coherent story: a double‑digit‑growth SaaS company that has crossed into profitability, is leveraging its scale to shape how AI agents are secured, and is using its platform, brand, and venture arm to anchor an entire identity‑adjacent ecosystem.

For an allocator deciding between “high‑beta AI plays” and “steady enablers,” Okta increasingly reads like the latter: less glamour, more governance, and—critically—more clarity on the path to margin expansion. In a world where AI is still a buzzword for many but a budget line for a few, that kind of narrative tends to age well on both sell‑side notes and SEO‑ranking pages.

Okta Announces Fourth Quarter and Fiscal Year 2026 Financial Results https://www.okta.com/newsroom/press-releases/okta-announces-fourth-quarter-fiscal-year-2026-financial-results/

Okta Announces $1 Billion Share Repurchase Program https://www.okta.com/newsroom/press-releases/okta-announces–1-billion-share-repurchase-program-/

Okta to Announce First Quarter Fiscal Year 2027 Financial Results on May 28, 2026 https://www.businesswire.com/news/home/20260501396369/en/

New Okta Innovations Secure the AI‑Driven Enterprise and Combat AI‑Powered Fraud https://www.okta.com/newsroom/press-releases/new-okta-innovations-secure-the-ai-driven-enterprise-and-combat-/

Okta Named a Leader in The 2026 Forrester Wave: Workforce Identity Security Platforms https://investor.okta.com/news-and-events/news-releases/default.aspx (select the May 21, 2026 release)

Okta Ventures – “The Identity 25” 2026 https://www.okta.com/okta-ventures/

Autodesk Inc. (NASDAQ: ADSK) just did something very on-brand for the AI era: it paid $3.6 billion in cash for a company that helps factories keep the lights on and the machines behaving. MaintainX, a modern maintenance and operations platform, is Autodesk’s biggest deal ever and a clear signal that “design software” is no longer enough in a world obsessed with data, uptime, and AI-driven efficiency.

In one move, Autodesk is stretching its moat from the CAD workstation all the way to the factory floor, promising investors a story that blends recurring revenue, operational stickiness, and AI buzzwords into a single neatly formatted slide. MaintainX expects more than $135 million in annual recurring revenue by 2026, growing north of 50%, which makes the purchase price rich but not irrational in a world where Wall Street still pays up for growth with a narrative attached.

From Blueprints to Broken Belts: The Strategic Logic

The industrial world has long suffered from an awkward custody battle: engineers design assets, construction teams build them, and then operations teams inherit the headaches. Autodesk now wants to own that entire arc, plugging MaintainX into a new Autodesk Operations Solutions division alongside tools like Fusion and digital twin platforms, creating a “design–build–maintain” loop that keeps customers inside the ADSK universe for years.

That matters because maintenance software is not a glamorous category, but it is a sticky one: once plant managers standardize work orders, inspections, and asset histories on a single system, ripping it out is about as appealing as shutting down a profitable production line for fun. For Autodesk shareholders, that translates into durable, high-margin subscriptions that are less sensitive to new-project cycles and more tied to the daily hum of global industry.

AI, Uptime, and the Investor Imagination

Autodesk is not just buying checklists and digital clipboards; it is buying an AI narrative that markets love. Management has been explicit that MaintainX will feed into AI-driven operational insights across Autodesk Operations Solutions, connecting real-world usage data back into design and optimization workflows.

In practical terms, that means the same ecosystem that helps design a facility could eventually recommend when to service a critical pump before it fails, how to reduce downtime, and where to squeeze more throughput out of existing assets—exactly the sort of “do more with what you already own” pitch CFOs like to hear when capital budgets are tight and investors are watching cash.

Financing the Future: Cash Now, Optional Multiple Expansion Later

Autodesk plans to fund the deal with roughly $1.6 billion in cash on hand and the rest via debt financing, a structure that keeps equity dilution off the table while modestly levering up the balance sheet. The acquisition is expected to close later this fiscal year, pending the usual regulatory formalities, giving investors several quarters to argue over whether Autodesk paid too much, exactly enough, or not nearly enough for a ticket into mission-critical operations.

On the upside scenario, if MaintainX sustains 50%+ ARR growth and Autodesk successfully cross-sells into its installed base, the multiple could look far more reasonable in hindsight—especially if management can demonstrate that connecting design and operations lowers churn and lifts net revenue retention across the platform.

Behavioural Finance, but Make It Literal

Interestingly, while Autodesk is buying operational data, academia is busy reminding investors that human behaviour is still the messiest variable in any model. Nature Human Behaviour, a multidisciplinary journal under the Nature Portfolio umbrella, has been spotlighting research that digs into how people actually make decisions—individually and in groups—often diverging sharply from the tidy rational-agent assumptions still lurking in older spreadsheets.

For markets, that kind of work is a quiet but powerful undercurrent: it informs everything from how investors react to M&A headlines to how workers in a plant adopt (or resist) new tools like MaintainX. It also shows up in how patients and clinicians embrace digital health platforms from companies such as Amwell (NYSE: AMWL), where the success of virtual care depends as much on trust, habit, and perception of convenience as on the underlying technology or reimbursement codes. It is a useful reminder that even the slickest AI-optimized workflow—or telehealth stack—ultimately runs through humans, with all their biases, shortcuts, and occasional brilliance.

FMC’s CFO Heads to the Conference Circuit

Meanwhile, over in chemicals and crop protection land, FMC Corporation (NYSE: FMC) is doing something much more traditional: sending its chief financial officer, Andrew Sandifer, to talk to investors. Sandifer, who serves as executive vice president and CFO, is slated to speak at the 16th Annual Wells Fargo Industrials & Materials Conference, with remarks accessible via webcast through FMC’s investor relations site.

For investors, these events are less about theatrics and more about nuance: tone on pricing power, commentary on agricultural demand, and hints about capital allocation priorities can all move a stock in ways that no slide deck alone can. In an environment where input costs, crop cycles, and geopolitics keep shifting, having a CFO who can explain the moving parts clearly is an underappreciated asse.

The Common Thread: Data, Discipline, and Narratives That Stick

Autodesk’s expansion into AI-enabled operations, FMC’s steady investor communication, and the behavioural insights emerging from Nature Human Behaviour all point toward the same meta-theme: markets are rewarding stories where data discipline meets human reality. Maintenance platforms that prevent costly downtime, management teams that can credibly frame their outlooks, and research that explains why people behave the way they do all feed into how capital is allocated—and reallocated—across sectors.

For investors, the magnetism here is not just in a $3.6 billion headline or a conference slot; it is in spotting where these threads converge: industrial software that becomes infrastructural, chemicals businesses that manage volatility with clear communication, and behavioural insights that help separate signal from noise.

The Sources

Autodesk acquires MaintainX for $3.6 billion in cash deal (Yahoo Finance) https://finance.yahoo.com/markets/stocks/articles/autodesk-acquires-maintainx-3-6-144836000.htmlfinance.yahoo

Autodesk to acquire MaintainX, advancing unified platform in operations (Autodesk Newsroom) https://adsknews.autodesk.com/en/news/autodesk-to-acquire-maintainx-advancing-unified-platform-in-operations/adsknews.autodesk

Autodesk bets big on AI operations with $3.6 billion MaintainX deal (Yahoo Finance – Technology) https://finance.yahoo.com/sectors/technology/articles/autodesk-bets-big-ai-operations-205835410.htmlfinance.yahoo

Autodesk Acquires MaintainX In $3.6 Billion Deal To Expand Operations Platform And AI Capabilities (Pulse 2.0) https://pulse2.com/autodesk-acquires-maintainx-in-3-6-billion-deal-to-expand-operations-platform-and-ai-capabilities/pulse2

Autodesk plans to acquire MaintainX for $3.6B (Seeking Alpha) https://seekingalpha.com/news/4598152-autodesk-plans-to-acquire-maintainx-for-3_6bseekingalpha

Nature Human Behaviour (journal overview) https://en.wikipedia.org/wiki/Nature_Human_Behaviourwikipedia

Nature Human Behaviour – journal badges and scope (Springer Nature Research Communities) https://communities.springernature.com/badges/nature-human-behaviourcommunities.springernature

FMC Corporation CFO Andrew Sandifer to speak at 16th Annual Wells Fargo Industrials & Materials Conference (press release via Morningstar/PR Newswire) https://www.morningstar.com/news/pr-newswire/20260526ph67769/fmc-corporation-cfo-andrew-sandifer-to-speak-at-16th-annual-wells-fargo-industrials-materials-conferencemorningstar

Andrew Sandifer – Executive Vice President and Chief Financial Officer at FMC Corporation (professional profile) https://www.marketscreener.com/insider/ANDREW-SANDIFER-A0EJOS/marketscreener

Andrew Sandifer – LinkedIn profile (background and role at FMC Corporation) https://www.linkedin.com/in/andrewdsandiferlinkedin

Wall Street spent the day toggling between blackjack odds and server racks, as investors tried to price a $17.6 billion casino roll‑up and Dell’s biggest growth spurt since it came back to the public markets. For once, the house and the hardware both seemed to be winning, and the tape looked more like a confidence vote than a coin toss.

Caesars Gets a New Boss: Fertitta Bets the House

Caesars Entertainment (CZR) is set to be acquired by Tilman Fertitta’s Fertitta Entertainment in a deal valued at about $17.6 billion, including debt, putting one of the largest casino operators on the Strip under the same roof as Golden Nugget and the Houston Rockets. The transaction, struck at a premium to prior takeover chatter that had circled around the low‑$30s per share, instantly vaults Fertitta from “interested buyer” to prospective kingpin of a Vegas empire that has already survived private‑equity ownership, a bankruptcy, and more than one reinvention.

Investors have seen versions of this movie before: leverage, consolidation, and a promise that scale will make the slot machines spin more profitably. But this time, the buyer is an operator with a long record of squeezing margins from both casinos and restaurants, and the strategic logic is less about financial engineering than welding together brands, loyalty programs, and real estate into a single, high‑limit ecosystem.

Change‑of‑Control: Fine Print at High Stakes

Behind the headline number sits a deck of covenants: an acquisition that hands Fertitta more than 50% of Caesars’ voting stock is likely to trigger change‑of‑control provisions in credit agreements and bond indentures. In plain English, that means lenders may get a say in how this deal is structured, forcing Fertitta’s team to consider tactics such as capping voting ownership at 50%, adding co‑investors, or assembling a “permitted holder group” to keep the legal tripwires from snapping.

For bondholders, the situation is less a panic than a negotiation opportunity: a formal change of control can mean put rights or better terms, but it can also mean a more levered balance sheet if the buyer decides to lean into debt. Equity investors, meanwhile, are weighing whether a seasoned casino owner’s operational playbook can offset the risks of higher leverage at a time when interest rates may not cooperate with Vegas‑style optimism.

Vegas Mood: Consolidation as a Feature, Not a Bug

The Caesars–Fertitta tie‑up underscores a broader theme on the Strip: size is becoming a defensive asset in an environment of volatile travel trends, rising wage costs, and increasingly capricious high‑roller demand. With multiple parties having circled Caesars in recent months—including private vehicles and talk of management‑led buyouts—this deal signals that casino real estate is far from exhausted as a financial asset class.

In that context, Fertitta is not just buying tables and towers; he is buying traffic, data, and cross‑sell options that span from regional properties to destination resorts. The strategic question isn’t whether the slot floors fill on a Saturday night, but whether a unified platform can extract one more night, one more convention, and one more high‑margin experience from the same customer base.

Dell’s Q1: When Boring PCs Go Full Growth Stock