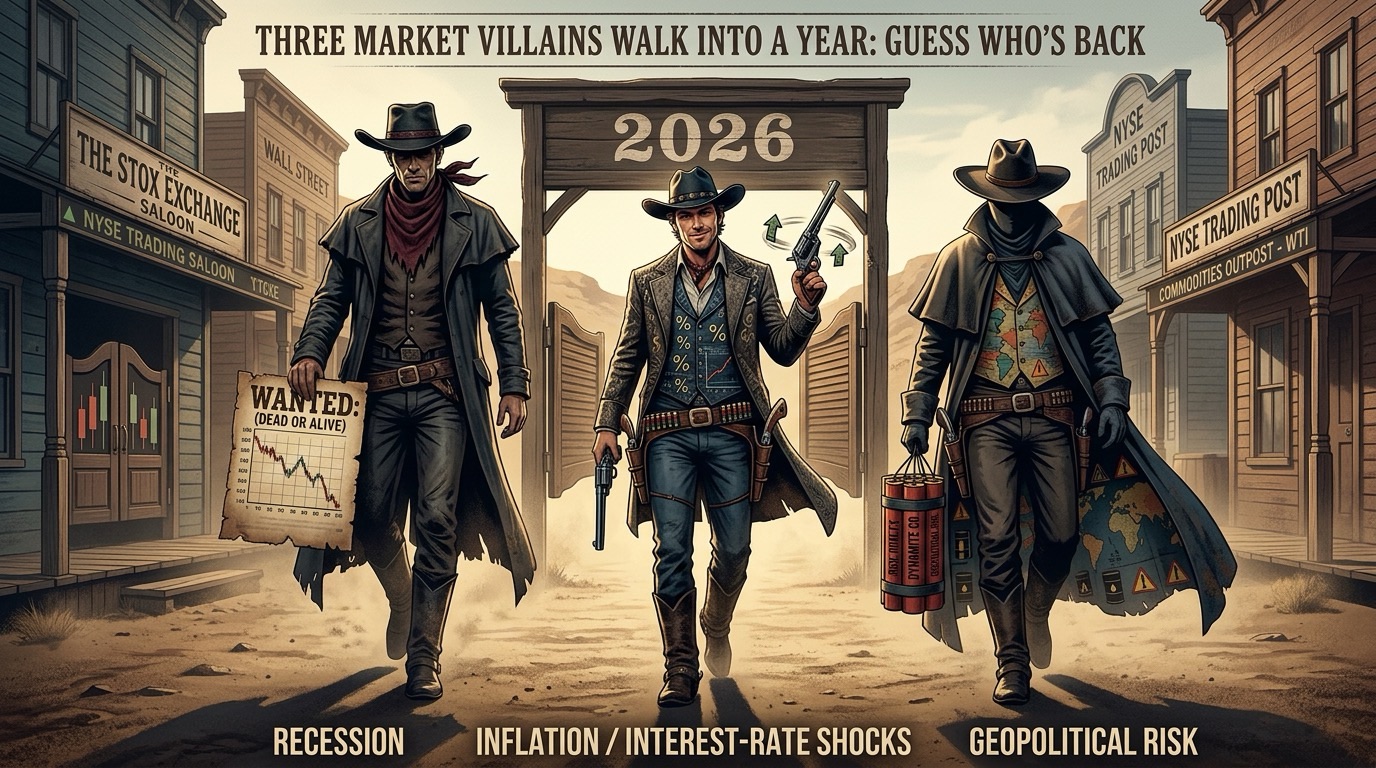

History may not repeat, but when markets stumble badly it does tend to recycle the same culprits. Over the last century, the ugliest calendar‑year stock market losses have usually traced back to one of three forces: recessions, inflation or interest‑rate shocks, and policy or geopolitical crises. In many downturns, investors only have to deal with one or two of those at a time, which markets can often muddle through with sharp but temporary dislocations. The truly painful episodes are the rarer ones when all three turn up at once and start reinforcing one another rather than offsetting the damage. That is the uncomfortable rhyme with today’s tape: each of those classic triggers is back in view, and they are no longer politely taking turns.

Three triggers, one uneasy backdrop

The first suspect is growth. While economists are still debating whether the US is heading for a formal recession or just a slowdown with a bad attitude, tighter financial conditions are clearly doing some work. Higher borrowing costs, more selective credit, and a cooler funding environment have started to pinch everything from small‑business hiring plans to parts of the consumer and housing complexes. Earnings expectations have held up reasonably well so far, but forward guidance has taken on a more cautious tone, and management teams sound far less certain that demand will stay bulletproof if rates stay elevated.

The second suspect is inflation—and its close cousin, interest‑rate risk. After investors spent much of the past year celebrating the prospect of imminent rate cuts, a string of sticky inflation readings has reminded markets that central banks do not get to declare victory just because everyone is bored of talking about prices. War‑driven energy costs are adding another layer of complication, with oil and refined products periodically spiking as the Iran conflict and broader Middle East tensions rumble on. Higher energy feeds into headline inflation and, more importantly, inflation expectations, forcing policymakers to keep the “higher for longer” option on the table. That is not the backdrop in which valuations get the benefit of the doubt.

The third suspect is policy and geopolitics. The US‑Iran conflict and its spillover effects on global trade routes, shipping insurance, and regional alliances have turned the geopolitical map into a live‑fire risk‑management exercise. Markets can live with bad news; what they hate is the combination of incomplete information and high escalation risk. Each new headline about ceasefires, strikes, or diplomatic flare‑ups pushes traders to re‑price not just energy and defense names, but risk appetite across the board. Layer on election calendars, shifting regulatory regimes, and policy debates over everything from capital requirements to tech antitrust, and “policy risk” starts to look less like a tail event and more like daily weather.

When all three of these forces line up, the result is a kind of cross‑asset stress test in real time. It is not just equities that feel the strain; bonds, gold, and even crypto have shown flashes of discomfort as investors try to hedge, de‑risk, and opportunistically buy the dip—often all in the same week. Correlations that were supposed to provide comfort can suddenly move toward one, and carefully constructed diversification stops working quite as well as the sales pitch suggested, at least temporarily.

Risk management, not surrender

The fact that all three triggers are “on” does not guarantee a deep bear market, but it does argue for more deliberate risk management. This is less a moment for drama than for discipline. For equity investors, that can mean revisiting how much of the portfolio is riding on the most speculative growth stories, particularly those whose valuations were built on a world of near‑free money. Stress‑testing positions against further rate back‑ups, wider credit spreads, or another leg higher in volatility is no longer a theoretical exercise; it is basic hygiene. It also means making sure liquidity needs are covered so that a spell of turbulence does not force sales at the worst possible time.

For diversified allocators, the toolkit is broader but the questions are similar. What role should cash and short‑duration bonds play as shock absorbers if both stocks and longer‑dated bonds come under pressure? Are defensive equity sectors still doing their job, or have they quietly morphed into crowded trades with less protection than advertised? Does the portfolio still reflect a conscious view on risk, or has it drifted into something more accidental over the last decade of falling rates and rising multiples?

The awkward truth is that managing through this kind of backdrop requires a higher tolerance for headline noise than most people find comfortable. But history also suggests that elevated volatility and rising risk premiums have a habit of leaving behind attractive entry points for investors who can tell the difference between cyclical drawdowns and permanent impairment. Periods when everyone suddenly remembers the three classic triggers are often the same periods when strong balance sheets, durable cash flows, and sensible valuations quietly go on sale. Using that window to upgrade quality—rather than simply shrink exposure—can pay off when the pressure eventually eases.

Why it matters

With the three traditional drivers of big market losses—recession risk, inflation and rate anxiety, and geopolitical or policy shocks—all flashing at once, this is a time to tighten risk management and sharpen security selection, not to assume that yesterday’s playbook will work on autopilot. Investors who stay level‑headed, focus on fundamentals, and treat volatility as a tool rather than a verdict will be better positioned if, as history often shows, the triggers eventually fade instead of compound.

Sources